From short-term investments to retirement planning, secure your future with smart financial strategies.

If you’re in your 20s or early 30s, chances are investing feels like something you’ll think about later in life. Maybe after you earn more, pay off a student loan, or finally “understand” the markets. However, you don’t need to be a financial expert or have a 6-figure income to start your investing journey. Just begin at the right time and with the right mindset.

The sooner you start, the safer it is to achieve your financial goals and get returns beyond expectations. If you begin with as low as ₹1,000/month at the age of 20, it can compound into almost ₹50 lakhs by the time you turn 60, assuming an expected return of 10%. This is why it is always advised to start planning retirement as early as possible, because the returns will compound even with a lesser amount. There are various short-term investments and long-term investment options available for young investors to begin with.

What Are Smart Investments for Beginners?

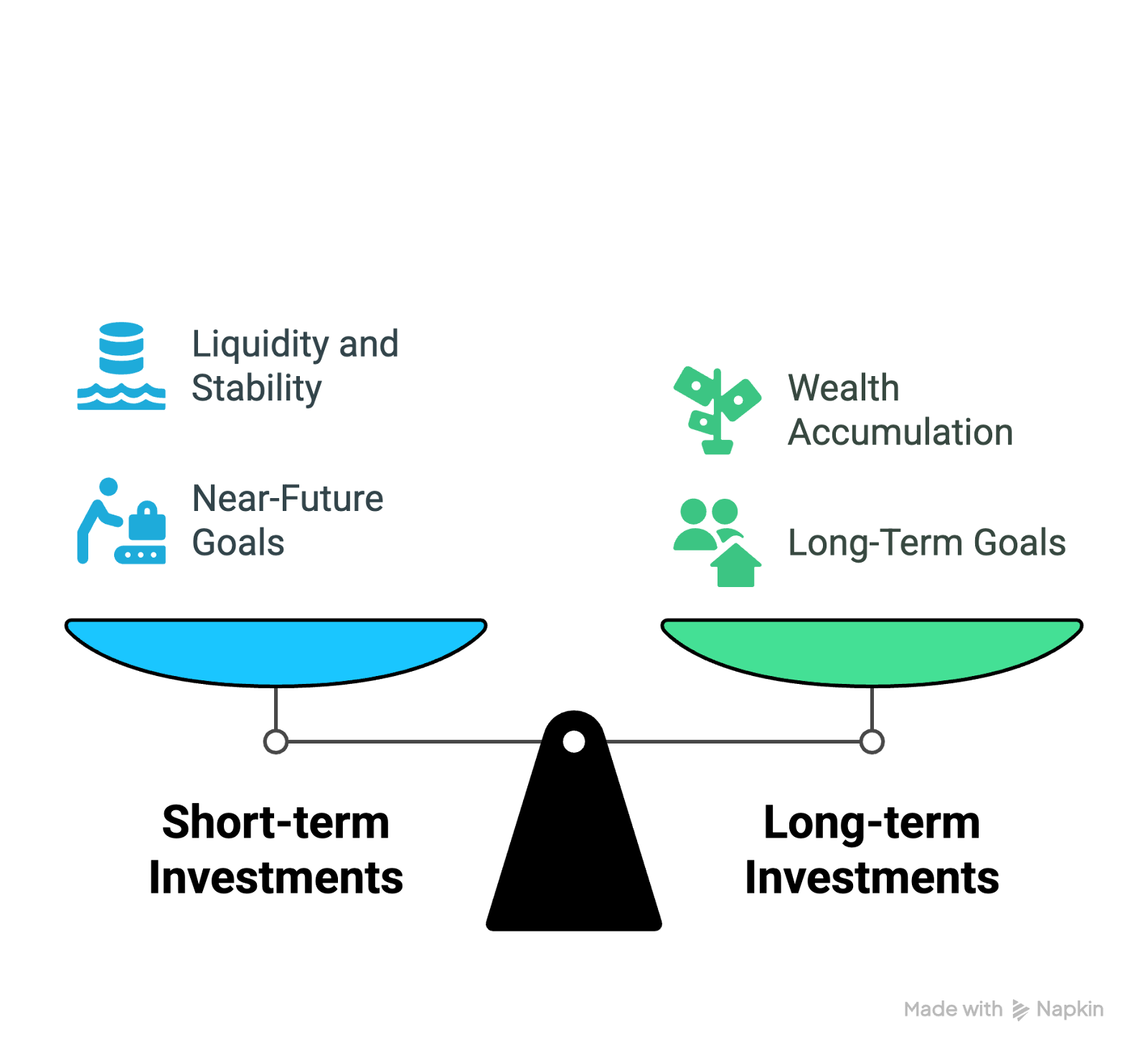

Time is the most valuable asset in investing. The fundamental principle of investing is to put your money to work so that it can grow with time. The wealth created can help in fulfilling various financial goals, such as buying a house, saving for a trip, or maybe investing for retirement. Depending on your investment expectations and goals, you may categorise your investments into three broad classes of Short-term investments, Medium-term investments, and Long-term investments.

- Short-term investments: These are investments for a short time, designed to offer returns in 1–3 years. These are ideal for near-future goals like saving for a car or building an emergency fund. These investments focus mainly on liquidity and stability.

- Medium-term investments: These investments are usually for 3-5 years of time period. Medium-term investments are for goals like higher education, saving for a big event or funding for a trip. These provide a balance between risk and returns.

- Long-term investments: These investments are for building wealth in over 5, 10, 20+ years. These are for bigger goals like retirement, buying a house, or funding your child’s education.

No matter what the goal is, the earlier you begin, the more opportunity and time your money has to grow for you.

Low-Risk, Beginner-Friendly Short-Term Investments

Below are some of the beginner short-term investment options available in the market. You can invest as little as ₹500/month in these investment avenues.

1. Liquid Mutual Funds

A liquid mutual fund is a type of debt mutual fund that invests in short-term debt instruments like treasury bills, commercial papers, and government securities. These instruments typically have a maturity period of up to 91 days. The short duration of these investments allows liquid funds to offer both safety and liquidity to investors. With easy withdrawal options and returns of around 5–6% annually, they’re ideal for emergency funds or short-term savings goals.

2. Recurring Deposits (RDs)

A recurring deposit is a banking instrument that allows you to invest a fixed sum of amount each month. RDs typically earn between 4.50% to 8% on investments and are a great choice for risk-averse investors.

3. Index Funds and ETFs

Though not traditionally “short-term,” index funds and ETFs are suitable for medium-term goals (3–5 years). These are capital market instruments that mirror the market indices like the Nifty 50 or Sensex and offer low-cost exposure to diversified equity markets.

Saving for Retirement: The Earlier, the Better

Retirement planning isn’t only for people in their 40s. It’s for everyone. If you start investing through an SIP with just ₹5,000/month at age 25 in a retirement-focused mutual fund, you can accumulate ₹1.5–2 crore by 60. That’s just ₹166/day- the cost of a daily coffee. However, these can be a little risky as they move with market volatility. Early contributions, even the smallest ones, can reduce the financial burden in your later years and maximize the benefits of compounding.

Most Popular Retirement Plan Choices in India:

- Mutual Funds: These are equity or hybrid funds tailored for long-term retirement needs. A systematic investment plan (SIP) of even ₹2,000-₹3,000 per month can grow into a substantial corpus over 25–30 years with an expected rate of return of 10-12%.

- Public Provident Fund (PPF): These are government-backed funds and are less risky with a 15-year lock-in. Returns are tax-free and currently around 7.1%. You can deposit a minimum of ₹ 500 and a maximum amount of ₹ 1.5 lakh in a financial year.

- Employees’ Provident Fund (EPF): This is a retirement-focused fund for employees. The amount for this fund is automatically deducted from the salary of an employee if they are working with a registered organisation. The employer also contributes, providing a powerful savings boost. The amount grows with an interest rate of 8.25% as of FY25.

- National Pension System (NPS): A voluntary retirement savings plan for young individuals. This pension scheme is a mix of equity and debt exposure. NPS is a low-cost, long-term investment with additional tax benefits under Section 80CCD(1B). Historically, NPS returns have averaged at almost 9-12%

Saving for retirement should ideally begin as you start earning. In India, you can choose from plenty of retirement plan choices. But the real value lies in the consistency of investing.

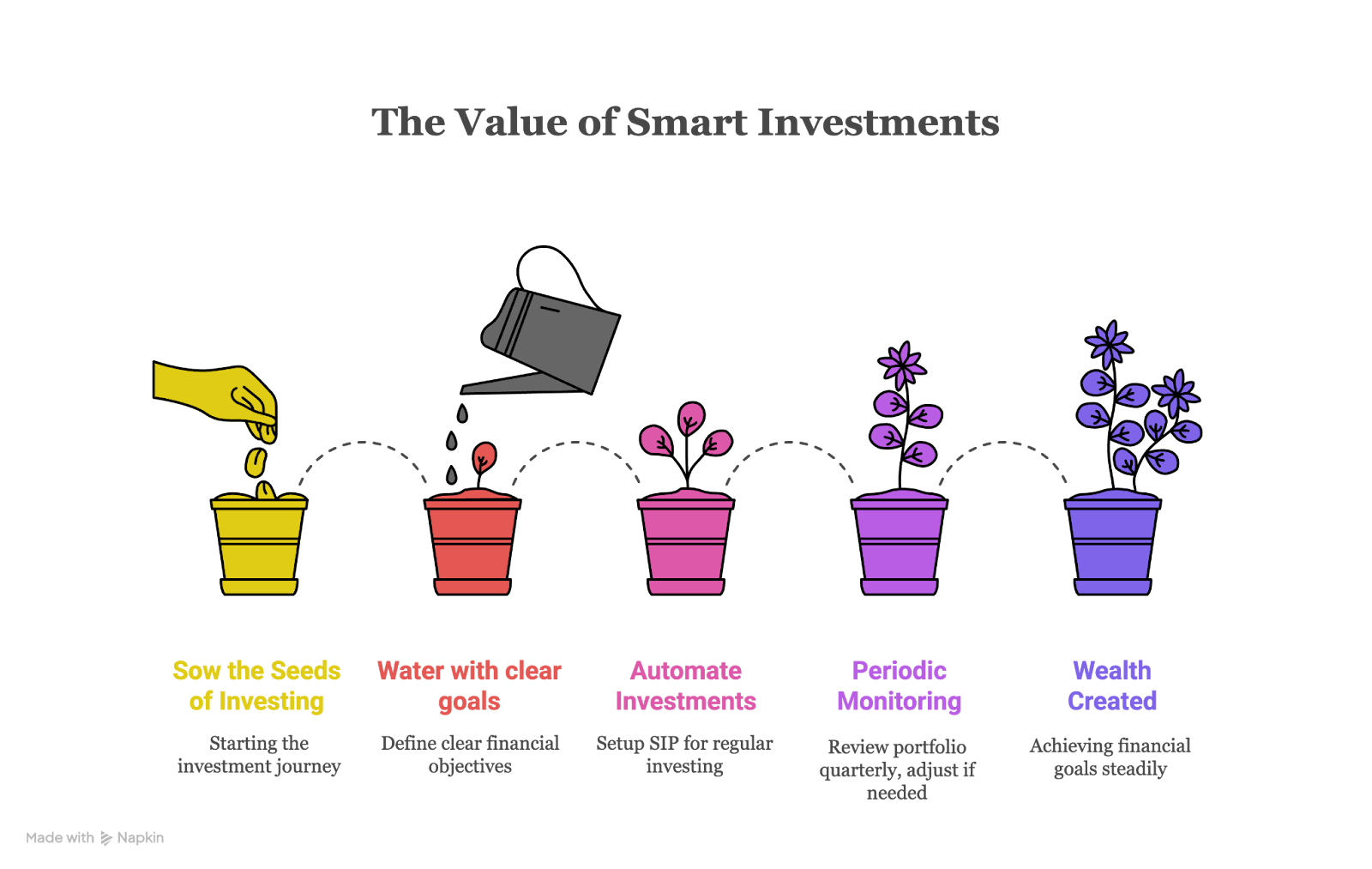

How to Begin Investing:

Wealth is created with small investing habits and consistent efforts. Investing is not an one-time activity. If you start early in your 20s, a smart investment habit begins with sowing the seeds with small investments.

Starting your investment journey doesn’t really require extensive market knowledge. A simple, structured approach can help you understand and get into the process confidently.

- Choose the Right Platform

Various financial platforms are available online to find information and invest in mutual funds, ETFs, and retirement schemes. You can begin by learning first and then start investing. - Define Financial Goals as Per Your Needs

Identify what you’re investing for, short-term investments like planning a trip or buying a gadget, medium-term goals like saving for a car or higher education, and long-term objectives like retirement or buying a home. Research about various options available on online platforms. - Automate via SIPs

Based on your financial goal, set up a Systematic Investment Plan (SIP) to ensure regular investment without manual effort. You can initiate with as minimum as ₹500–₹1,000 per month. - Monitor Periodically

Refrain from checking your portfolio daily, as the market movements may lower your confidence. Review it quarterly to ensure you’re on track and adjust as per the market conditions or your goals.

Choose Smart Investing

Investing is just one piece of the whole financial puzzle. But to achieve tangible results, one needs to develop smart money habits to go along with it. Begin with the 50-30-20 rule: spend 50% on needs, 30% on wants, and the rest 20% on savings and investments. This structure can help in building a regular monthly practice of investing and not just an action that you are trying to squeeze in. Additionally, refrain from getting into heavily aggressive investments before paying off high-interest debt, such as credit card balances. The potential market returns are usually outweighed by the interest saved here.

Once you have established your goals, examine them at least once a year as long as you grow professionally and financially. Rebalancing your portfolio, readjusting SIP amounts, or prioritizing short-term and long-term objectives are some ways to keep your financial plan in the best alignment with you. Investing wisely is not only about putting funds in the right scheme but also about managing it deliberately.

- Forex Trading for Beginners: Strategies, Risks & Profits - April 7, 2026

- Make in India 2.0: How Manufacturing Is Reshaping Market Sentiment - December 13, 2025

- Real Estate Boom : Why Tier-2 Cities Are Attracting Big Investors - December 12, 2025