Table of Contents

Not receiving responses from your bank to resolve your issues? Worry no more, here is a special authority to help you.

Have you faced a situation of banks not responding to your queries and concerns? If yes, the concept of a banking ombudsman is essential for you.

Though we are more aware as customers today, not all of us are familiar with the term “banking ombudsman”.

The original introduction of this scheme was in 1995. The scheme has undergone multiple updates post-1995, to suit the growing requirements of banking customers.

Banking Ombudsman

A banking ombudsman is an official representative of the government and the Reserve Bank of India (RBI). The role of this official is to handle customer complaints and grievances that do not get appropriate resolutions from financial institutions.

A customer can seek the help of a banking ombudsman if the financial institution does not resolve the concern within 30 days. Even in cases where the bank’s resolution is not convincing to customers, they can reach out to the banking ombudsman.

Some interesting statistics

India has 22 offices where the banking ombudsmen sit. The number of complaints received in 2021-22 is 4,18,184, compared to 3,82,292 complaints in 2020-21, showing an increase of 9.39% YoY.

The city with the highest number of complaints in 2021-22 was New Delhi, followed by Mumbai and Kanpur.

The relevance of this scheme to customers

The idea behind this scheme was to create a quasi-judicial authority to provide cost-efficient and timely assistance to customers.

The formation of the scheme in 1995 was under the Banking Regulation Act of 1949. The RBI issued an amendment in 2021, combining all the regulations listed in the older plans. Integrated Ombudsman Scheme, 2021 has all the rules relevant to banking ombudsmen today.

Below are the types of banks falling within the purview of banking ombudsman:

- Commercial Banks

- Foreign Banks having Indian business.

- Scheduled Primary Co-operative Banks and Non-Scheduled Primary Co-operative Banks having deposit size of ₹50 crores and above

- Regional Rural Banks (RRBs)

- Non-Banking Financial Corporations (NBFCs).

Issues handled by the banking ombudsman

Customers can approach the ombudsman for various issues. Some of them are listed below:

- Unusual delays or failure on the part of the bank to clear/collect cheques and other bills

- Rejecting payments made in currencies of small denomination unless there is a genuine reason or charging commission to accept it

- Banks not adhering to their work timings

- Non-fulfillment or delay by banks to execute promises given in writing

- When there is a delay in crediting the interest amount on deposits based on the rate of interest issued by RBI

- Complaints from NRIs (Non-Resident Indians) concerning their Indian bank accounts and related transactions

- When banks deny opening deposit accounts or force close them without genuine reasons and prior intimation

- New and additional charges to the customer without advance information

- Not following the RBI guidelines about ATMs, debit and credit cards, mobile banking, etc.

- Delay in pension-related payments

- Delay or refusing to accept tax payments made by customers without genuine reasons

- Issues related to banks not providing the necessary service regarding government securities

- Denial or delay to close accounts upon customer’s request

- When banks do not follow fair practices and RBI guidelines for recovery agents, mutual funds, insurance and other investment dealings

Consider the following points before going to an ombudsman

Banking ombudsmen have the authority to reject complaints if they notice a violation of any of these factors:

- Banks and other financial institutions are the first point of contact in resolving disputes. So, customers should reach out to their respective banks for resolution and then go to the ombudsman if they are not convinced.

- Customers must wait for 30 days to receive a response from banks before going to the ombudsman. If the reply is not satisfactory, they must reach out to the ombudsman within one year of receiving the response. If there is no reply from banks, they must approach the ombudsman within one year and 30 days of writing the complaint.

- The language and the tone used in the complaint must not be abusive.

- The current complaint can be rejected if it has already been handled by another forum or has been handled by the ombudsman in the past.

Lodging a complaint

A customer can write a letter and physically hand it to the banking ombudsman in the regional office. Customers can also apply online on the website https://cms.rbi.org.in or write an email to CRPC@rbi.org.in.

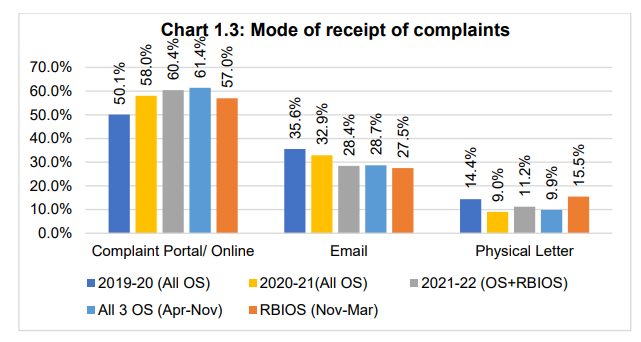

The below chart shows some data about the modes of complaints received.

Conclusion

A facility given by the government and the central bank of the country, Banking Ombudsmen are present across various states to aid customers in handling grievances related to banks and other financial institutions.

As customers, we must know our rights and use the facilities provided to us by the government. It is also significant for customers to preserve all necessary documents before going to an ombudsman.

DISCLAIMER: This article is not meant to be giving financial advice. Please seek a registered financial advisor for any investments.

- Section 80C Investments: Complete List to Maximise Tax Savings - July 8, 2026

- Top 10 Stocks to Watch in India: June 2026 - July 2, 2026

- India GDP Growth 2026 – What the Numbers Mean for Your Money? - July 2, 2026