India’s economy is one of the fastest-growing global economies with a constantly modernising and growing investment landscape. It is characterised by a growth of retail investment across various instruments, and a primary cause of this trend is the democratisation of investment due to digitisation. Therefore, if you have not begun your investment journey yet, this blog aims to list the most popular investment mediums, varying in their risk-return profile and other features, to help you choose the best investment options for 2026.

1. Stocks

Stock market investment implies investing in the shares of listed companies. A unit of ownership in the business is represented by each share. For example, if X buys 10 out of 100 shares of a company, he becomes the owner of 1/10th of the company. It is among the key high-return investments in India, and thus has a high risk profile.

As equity assets, stock investments are ownership interests and thus sit below debt in the repayment ladder. This means that if a company winds up its affairs, its creditors will be repaid first, and any amount left over will be returned to stockholders.

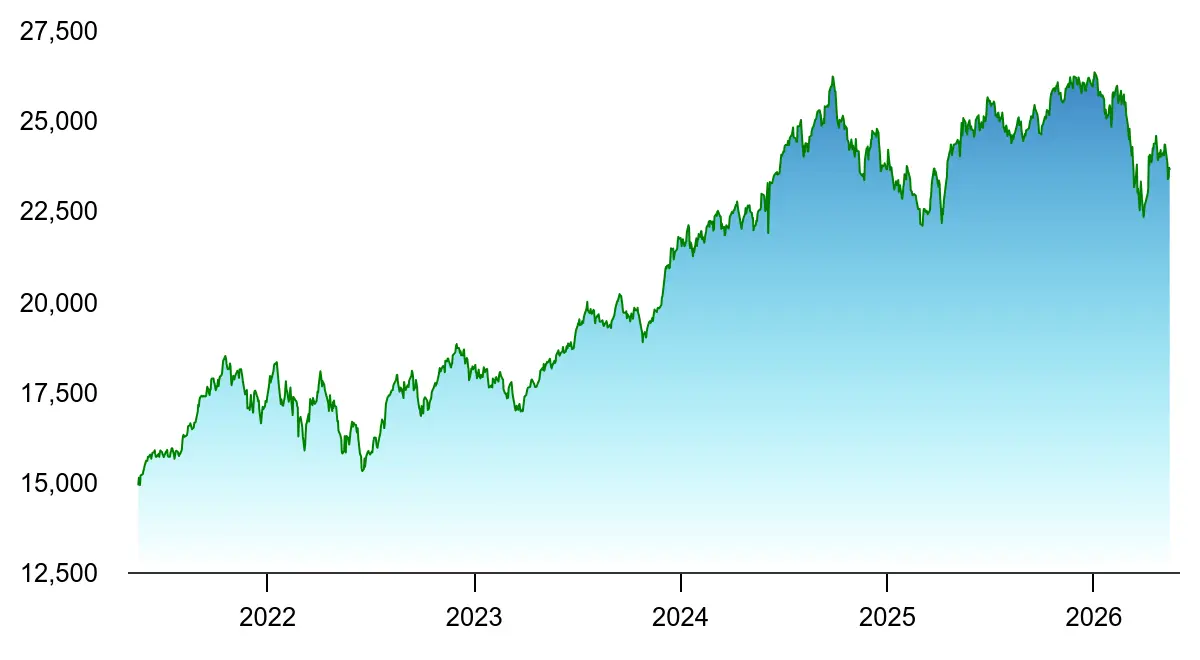

Flagship stock market indexes like Nifty 50, BSE Sensex, etc., act as standards or benchmarks that indicate overall market performance. If an investor wants to invest in stocks of a particular industry, then an index related to the industry can be used. Like Bank Nifty indicates the performance of banking sector stocks. The graph below shows the performance of Nifty50 as of 16 May 2026.

2. Mutual Funds

An investment medium that pools the investible corpus of individual investors to diversify across a range of assets, as specified in their fund sheet, is called a mutual fund. Experienced portfolio managers strategise and invest the corpus, according to the claimed portfolio mix. SEBI categorises mutual funds into different categories based on their asset allocation. But generally speaking, there are hybrid, debt, and equity mutual funds.

While equity funds primarily invest in equity and related instruments, debt funds invest in debt assets like bonds, money market securities, etc. Hybrid funds make investments in both. This portfolio allocation determines the average return and risk profile of a fund. For instance, equity funds are expected to offer greater returns at higher risk than debt funds.

The table below shows the key category average performance of popular mutual funds as of 16 May 2026.

| Mutual Fund Performance | Category Performance | |

| 3 Years (%) | 5 Years (%) | |

| Large-cap fund | 11.95 | 11.87 |

| Small-cap fund | 18.99 | 19.05 |

| Corporate bond fund | 6.71 | 5.89 |

| Dynamic asset allocation fund | 10.74 | 9.73 |

3. Bonds

One kind of fixed-income financial instrument that businesses, governments, and government agencies issue to raise money is a bond. Unlike equity, when investors invest in bonds, they become the creditors of the issuer. This asset provides a fixed-income opportunity, as the issuer pays interest on the debt and on maturity, the principal is repaid. Furthermore, there exists a secondary market for bonds where investors can sell their bond holdings before maturity at the prevailing rate to make capital gains.

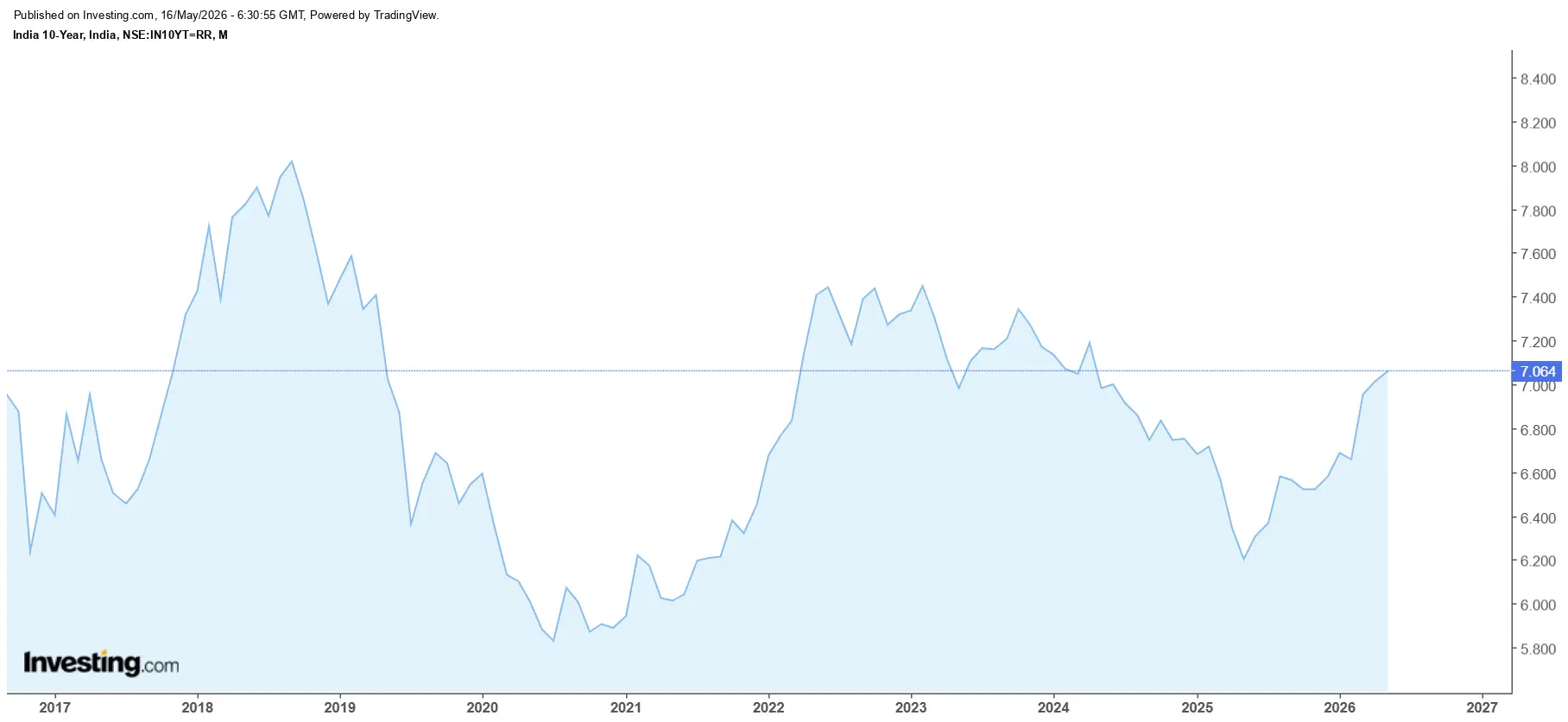

Bonds issued by private companies are called corporate bonds, while those issued by the central government, state government, or state-owned bodies are called government bonds. The graph below shows the India 10 Year Bond Yield, as of 16 May 2026.

4. Fixed Deposits

Banks allow investors to deposit a lump sum for a fixed tenure and interest. This is called a fixed deposit. It is among the conventional investment mediums in India that offer fixed returns, irrespective of market movement. Both private and government banks, NBFCs, small finance banks, etc., offer fixed deposits. However, similar to any investment, FD interest is proportional to risk. Therefore, usually, the returns of NBFC or small finance bank deposits are usually higher than private bank deposits, which in turn exceed public bank deposits.

Additionally, bank deposits up to INR 5 lakhs are insured for each investor by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a wholly-owned subsidiary of RBI. This enhances the low-risk profile of FDs.

5. Public Provident Fund

A government-backed, long-term savings investment tool, which offers fixed interest and is targeted for retirement planning, is called the Public Provident Fund (PPF) scheme. Investments in this asset can begin with INR 500, and investors can invest up to INR 1,50,000. There is a 5-year lock-in, and the PPF account matures after 15 fiscal years post the end of the year in which the investment was commenced. However, even after maturity, the account can be retained at the prevailing interest rate, but new contributions cannot be made. From 01 April 2020 to 30 June 2026, the PPF interest rate was 7.1%.

Deposits made to PPF enjoy tax benefits under Section 80C of the Income Tax Act, while the interest earned is also tax-free under Section 10 of the IT Act.

6. National Pension System

Regulated by the National Pension Regulatory and Development Authority, the National Pension System (NPS) is a government-backed, market-linked, voluntary retirement scheme designed to build a pension corpus for retirement. It works similar to mutual funds, where investors invest an amount periodically, and the accumulated corpus is invested into an equity, debt, and hybrid mix, as per the choice of the investor. The investment options available to investors are displayed in the table below.

| Active choice: Investors themselves plan and choose their asset allocation. | |

| Asset Class | Maximum Investment |

| Equity and related assets (E) | Up to 75% |

| Corporate Debt and related assets (C) | Up to 100% |

| Government bonds and related assets (G) | Up to 100% |

| Alternative Investment Fund (AIF) | Up to 5% |

| Auto choice: Investment in life cycle funds, wherein the asset allocation automatically adjusts with age. As age increases, exposure to assets like equity decreases. | |

| Asset | Risk |

| Life cycle 75 | High |

| Life cycle 50 | Moderate |

| Life cycle 25 | Low |

| Life cycle | Aggressive |

At maturity, investors must deposit at least 40% of proceeds in an annuity plan, but they can take up to 60% in one lump amount. An NPS investment falls under the Exempt Exempt Exempt category because the contributions, investment growth, and maturity have tax-exempt benefits.

7. Senior Citizen Savings Scheme

Senior people can receive a set rate of interest under the government-backed Senior Citizen Savings Scheme (SCSS). Investors who are 60 years of age or above 55 years but less than 60 years and retired under superannuation, VRS, special VRS, etc., can invest in SCSS. Investments can begin with INR 1,000, and the maximum contribution can reach up to INR 30 lakhs. Investors have the option to prolong the account for a further three years after the usual maturity of five years. The deposits can get deductions due to Section 80C. From 1 April 2023 to 30 June 2026, the declared interest rate is 8.20%.

8. Gold

Gold serves as a safe-haven asset that gains during times of turmoil, providing a hedge. Amid the growing geopolitical uncertainty, economic crisis, etc., around the world, gold has appreciated significantly in recent years. Investors can dedicate a proportion of their investible corpus to gold to ensure portfolio stability. Investment in gold can be made through several medium. However, while physical gold like jewellery, coins, bars, etc., can have making charges and storage costs that reduce their investibility, digital investment in assets like gold ETFs, mutual funds, sovereign gold bonds, etc., can provide a hedge, whilst reducing overhead costs.

9. Real Estate through REITs

Real Estate Investment Trusts, or REITs, are businesses that own, manage, or finance real estate that generates revenue. They work similarly to mutual funds for real estate, pooling the capital of several investors and investing in commercial real estate. Investors receive a portion of the rent collected from these buildings as returns. REIT units also trade on the stock exchange, giving secondary market access to investors, which increases liquidity. Therefore, through REITs, investors can gain capital growth without having to deal with the hassle of physically purchasing or managing properties.

10. Unit-Linked Insurance Plans

A hybrid financial instrument called a Unit Linked Insurance Plan (ULIP) combines market-linked wealth creation and life insurance into a single integrated plan. A portion of the premium is used to buy life insurance, while the rest is invested in stocks or debt funds. Therefore, investors can not only gain capital appreciation but also insurance coverage.

Goal-Based Investing

Investment decisions must be guided by parameters like risk appetite and investor objectives. Goal-based investing ensures that the assets chosen for investment align with the goals that the investor wishes to achieve. The table below discusses the different assets that investors often choose for particular goals.

| Goals | Explanation | Assets |

| Growth | Investors often choose high-return, high-risk assets to maximise capital | Stocks, equity mutual funds, etc. |

| Fixed-income | Earn a fixed income periodically | Bonds, fixed deposits, etc. |

| Retirement | Build a corpus for retirement | NPS, PPF, etc. |

| Emergency fund | Build a corpus to meet unexpected capital needs | Liquid assets or short-term investment options in India, like deposits in a savings account |

However, simply investing based on goals is not enough.

Bottomline

Investors must ensure optimal diversification of funds across different asset categories of varying risk and return metrics to ensure portfolio stability. For instance, even if the goal of an investor is growth, they can allocate a portion to fixed-income and liquid assets to reduce the risk. Therefore, allocation across the different top investment opportunities in 2026 can help balance growth, stability, hedge during a crisis, retirement needs, etc.

- Retirement Planning in India- How to Retire Comfortably by 60? - July 16, 2026

- How to Rank Financial Content on Google Without Triggering YMYL Penalties - July 16, 2026

- How to Build Trust as a Finance Brand Through Content Marketing - July 13, 2026