Looking for a simple way to grow your wealth?

In India, mutual funds are becoming a popular alternative to traditional savings avenues like bank FDs and gold. However, a lack of awareness has somewhat limited their widespread adoption.

The Indian mutual fund industry offers a variety of schemes tailored to different investment goals, whether it’s saving for retirement, education, or buying a home.

What is a mutual fund?

A mutual fund is like a large pot, where many investors put their money together. This pot is then managed by a professional called a Fund Manager.

The manager uses this collective fund to invest in various assets like stocks, bonds, and other assets. The goal? To make more money from these investments.

How do mutual funds work?

Imagine a group of friends who want to buy a large pizza, but each can only afford a slice. They pool their money to buy the whole pizza and then share it.

Mutual funds operate similarly. Your money joins that of other investors to buy a portfolio of investments. The returns from these investments are shared among all after deducting some expenses.

Similar to how each equity share has a specific trading price, every unit of a mutual fund has what is known as a Net Asset Value, or NAV per unit. It’s similar to calculating the cost per slice of the pizza.

NAV is determined by subtracting the mutual fund’s expenses from the total value of its investments and dividing this figure by the number of units in the fund.

This NAV per unit reflects the current market value of all the units in a mutual fund scheme on any particular day.

Types of Mutual Fund Schemes

Understanding the different types of mutual fund schemes is crucial in making informed decisions. Let’s break them down in simple terms.

Open-ended and closed-end funds

Open-end funds are like your everyday savings account. You can put in and take out money anytime. They don’t have an end date, making them quite flexible.

Closed-end funds, on the other hand, are more like fixed-term deposits. You can invest only during the initial offer period, and they have a fixed maturity date.

You can’t just take your money out whenever you want. Instead, these funds are listed on a stock exchange, and you can sell your units there if you need to exit before the fund matures.

Actively managed and passively managed funds

In an actively managed fund, the fund manager plays a hands-on role.

They constantly make decisions about what stocks to buy, sell, or hold, aiming to get the maximum returns and beat the benchmark. It’s a proactive approach to managing your investment.

Passively managed funds are the opposite. Here, the fund manager doesn’t make frequent changes. The goal is to mirror a market index, like the Sensex of Nifty.

They replicate the index exactly as it is, aiming to match its returns, not beat them. This approach is more about following the market’s overall trend without trying to outsmart it.

Categories of open-ended mutual funds

When diving into open-ended mutual funds, it’s crucial to understand the different categories based on their investment objectives and underlying securities. Here’s a breakdown:

Equity mutual funds

These funds mainly invest in company stocks. Since they’re typically more volatile, they’re better suited for long-term investments (over five years). There are various types within this category:

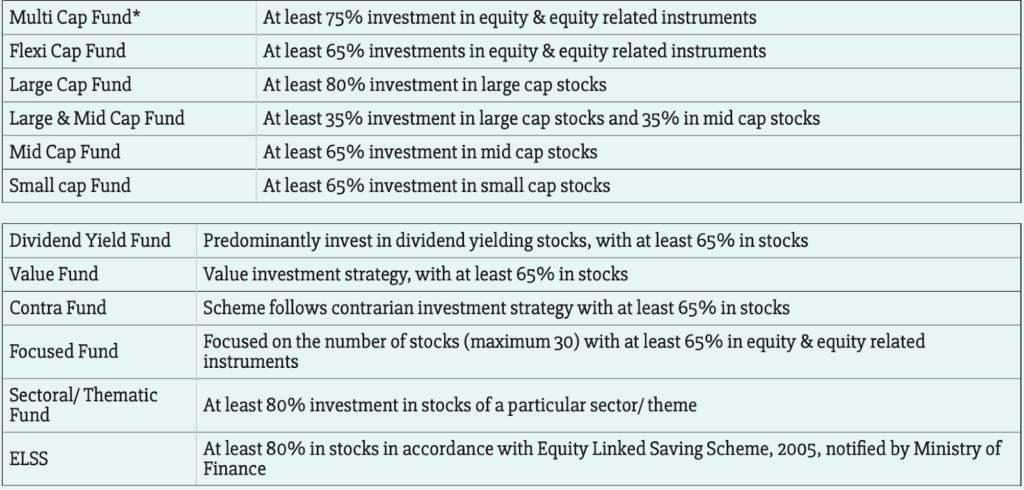

- Large-cap funds: Invest mostly in large, well-established companies.

- Mid-cap funds: Focus on medium-sized companies.

- Small-cap funds: Target smaller companies.

- Equity-Linked Savings Scheme (ELSS): These are tax-saving funds with a three-year lock-in period. Investments in ELSS qualify for tax benefits under Section 80C of the Income Tax Act.

- Multi-cap Funds: Invest in companies of all sizes.

- Index funds: Aim to replicate the performance of a market index, like the Sensex.

- International funds: Invest in foreign companies, offering geographical diversification.

Debt Mutual Funds

These funds invest in fixed-income instruments like government bonds and debentures. They offer more stable returns compared to equity funds and are less affected by stock market volatility. Key types include:

- Liquid funds: Invest in highly liquid instruments with a maturity of less than 91 days. Ideal for parking emergency funds.

- Short-duration funds: Maintain a duration of one to three years, investing in a mix of government and corporate bonds.

- Overnight funds: Invest in securities maturing in one day, hence very low risk.

Hybrid Mutual Funds

These funds combine equity and debt investments, offering a mix of growth and stability. Types include:

- Aggressive hybrid funds: Invest more in equity (65-80%) and the remainder in debt, sometimes using arbitrage opportunities.

- Conservative hybrid funds: Focus more on debt (75-90%) with a smaller equity component, offering greater security.

- Balanced advantage funds: Adjust equity and debt allocations based on market conditions to balance risk and reward.

Ways of investing in mutual funds

Mutual funds offer varied options to match individual investment goals. Let’s dive into three key strategies:

Systematic Investment Plan (SIP)

A SIP allows you to invest a fixed amount regularly in a mutual fund scheme. It’s a disciplined approach to investing and is particularly effective in the long term. SIPs help in managing market volatility by averaging the investment cost over time.

Suppose you start a SIP of ₹5,000 per month. During market dips, this amount will buy more units, and during highs, fewer. Over the years, this can average out your investment cost and potentially enhance returns.

Systematic Transfer Plan (STP)

An STP is a smart choice if you have a lump sum amount invested in a relatively safer fund, like a debt fund, and wish to move to an equity fund over time. It involves periodically transferring a set sum from one mutual fund to another.

If you have ₹2 lakhs in a debt fund, you could set up an STP to transfer ₹10,000 every month into an equity fund. This approach balances the safety of debt funds with the growth potential of equity funds.

Systematic Withdrawal Plan (SWP)

For those who need a regular income, such as retirees, a SWP is an ideal strategy. It involves withdrawing a specific amount from your mutual fund investment at regular intervals.

If you have a substantial sum in a mutual fund, you might set up an SWP to withdraw ₹10,000 every month. This provides a consistent income flow and can be a tax-efficient withdrawal strategy.

These investment strategies in mutual funds cater to diverse needs, from building wealth to ensuring a steady income post-retirement. Whether you are just starting your investment journey or looking for ways to manage your savings in retirement, mutual funds in India offer a flexible and effective avenue for your financial goals.

Conclusion

Mutual funds are a great choice for those who don’t have a large sum to invest upfront or prefer not to engage in daily market analysis.

By investing in mutual funds, you let experts manage your investments for a small fee, which is regulated to ensure fairness. However, selecting the right mutual fund is essential.

It involves understanding the risks, considering your investment duration, and possibly seeking advice from a financial expert.

DISCLAIMER: This article is not meant to be giving financial advice. Please seek a registered financial advisor for any investments.

- Section 80C Investments: Complete List to Maximise Tax Savings - July 8, 2026

- Top 10 Stocks to Watch in India: June 2026 - July 2, 2026

- India GDP Growth 2026 – What the Numbers Mean for Your Money? - July 2, 2026